Capital Is Flowing Back Into Oil & Gas, But Main Street Energy Is Still Looking for Its Seat at the Table

For the better part of a decade, the story in U.S. oil and gas has been one of consolidation. While capital is returning to energy, it is not being distributed evenly—independent buyers are finding unique opportunities in producing assets, minerals, royalties, and niche operating strategies.

For the better part of a decade, the story in U.S. oil and gas has been one of consolidation.

Large public companies became larger. Private equity-backed operators merged into billion-dollar platforms. Wall Street demanded capital discipline, free cash flow, and shareholder returns instead of aggressive production growth.

That strategy has largely worked.

Today, many public operators are generating stronger balance sheets than at any point in recent memory. Investors who remained in the sector have been rewarded, and energy has once again become a meaningful source of cash flow in institutional portfolios.

Yet beneath the headlines about billion-dollar mergers and corporate consolidation, a different story is unfolding.

The independent oil and gas operator is still very much alive.

According to Enverus, U.S. upstream M&A activity reached approximately $38 billion during the first quarter of 2026, marking the strongest start to a year since 2023.

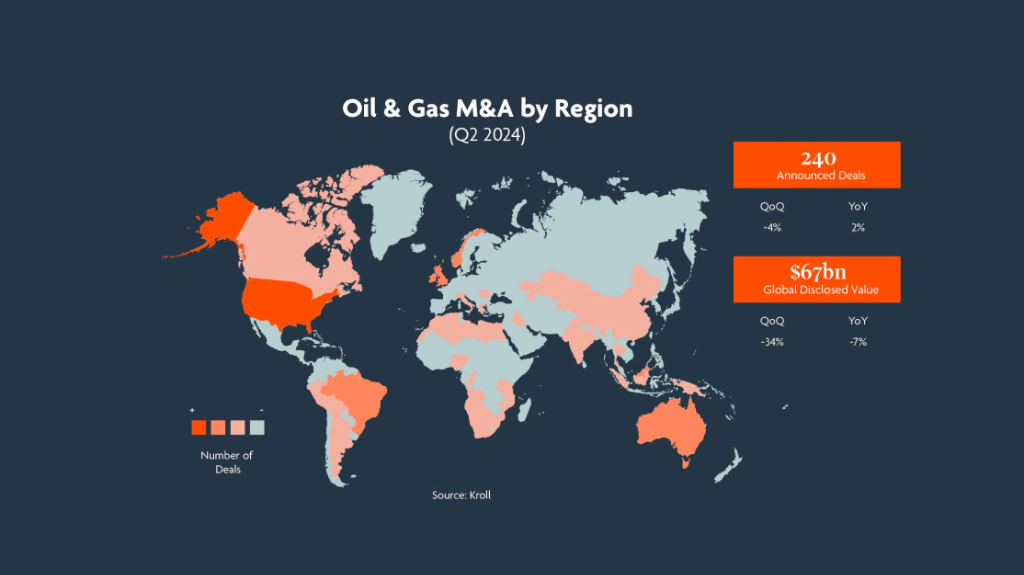

*Figure 1: Global Oil & Gas M&A deal count and disclosed value by region. Source: Kroll.*

The headline transaction was Devon Energy's merger with Coterra. But beyond the large deals, there remains significant activity among smaller operators, private companies, family offices, and entrepreneurial management teams looking to acquire producing assets.

In many cases, these buyers are not attempting to build the next publicly traded energy giant.

They are looking for something much simpler.

**Cash flow.**

For decades, independent operators have built businesses around acquiring overlooked producing properties, optimizing operations, reducing overhead, and generating reliable income from mature assets.

That model has not disappeared.

If anything, it may become increasingly important.

One reason is the changing nature of capital itself.

While institutional investors have returned to energy, they have become significantly more selective. Capital today is flowing toward scale, infrastructure, LNG projects, royalty businesses, and operators with demonstrated operational discipline.

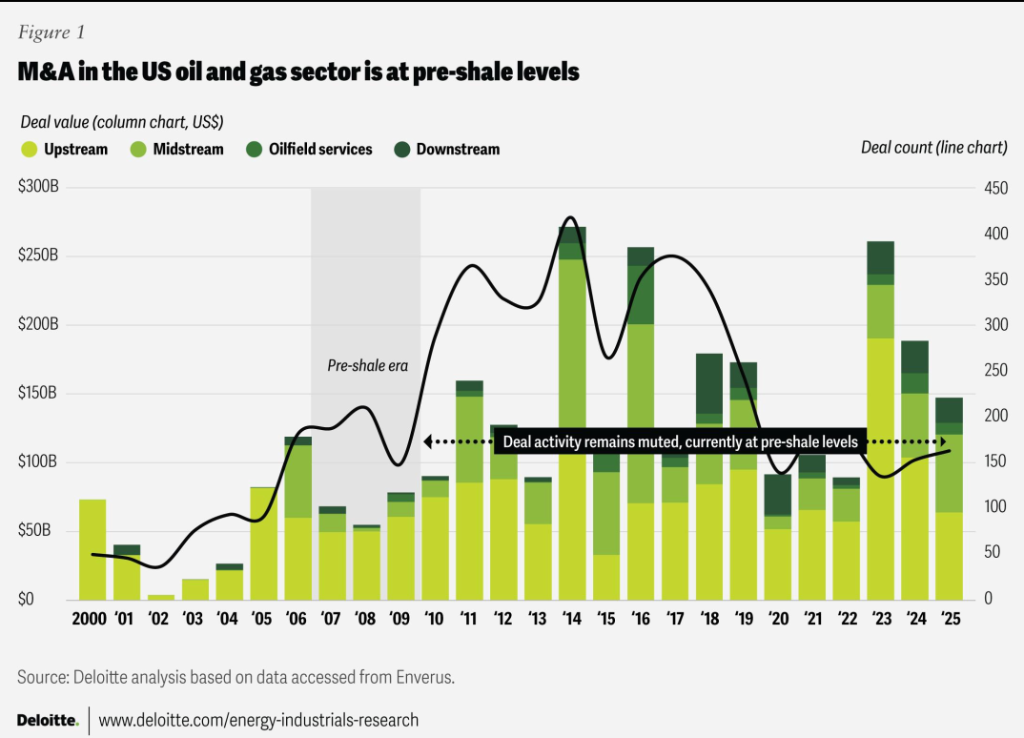

*Figure 2: M&A activity in the US oil and gas sector remains muted at pre-shale levels. Source: Deloitte.*

The days of raising hundreds of millions of dollars to drill acreage simply because oil prices are rising appear largely behind us.

That does not mean opportunities have disappeared.

It means opportunities have shifted.

Private buyers are increasingly evaluating PDP packages, non-operated interests, mineral portfolios, water infrastructure assets, and mature producing properties that can generate immediate cash flow.

In many cases, these transactions are being completed by groups that would never appear in a Reuters headline.

* Family offices.

* Local investment groups.

* Independent operators.

* Industry veterans.

* Groups of engineers and geologists who understand a basin better than any spreadsheet ever could.

Those buyers continue to play a critical role across Texas, Oklahoma, Louisiana, New Mexico, and Appalachia.

At the same time, another trend is emerging.

Natural gas is rapidly becoming one of the most important investment themes in North American energy.

The International Energy Agency recently projected that global natural gas investment will exceed $330 billion in 2026, reaching its highest level in more than a decade.

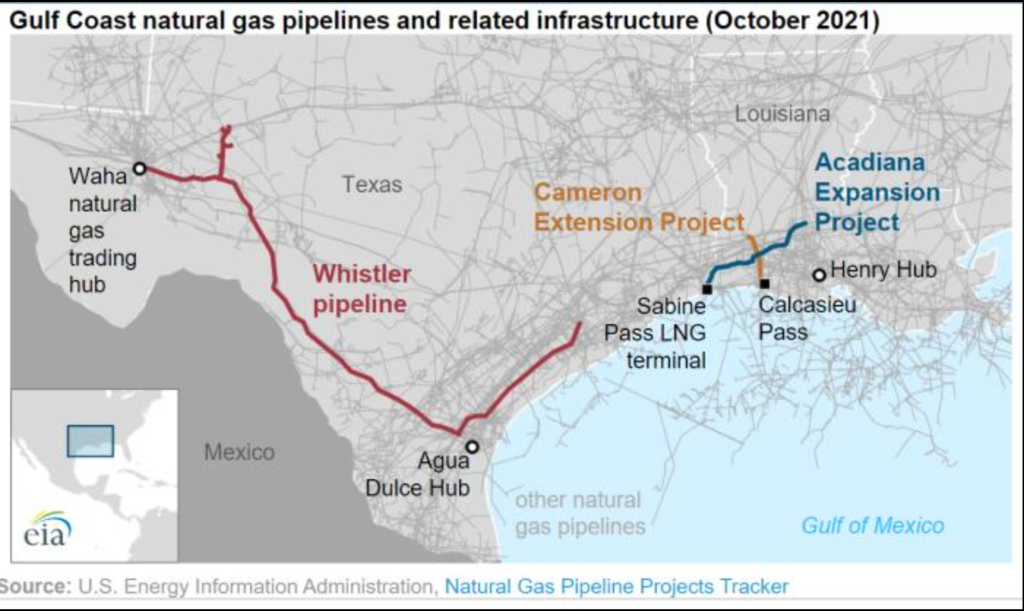

*Figure 3: Gulf Coast natural gas pipelines and related LNG infrastructure. Source: EIA.*

LNG export growth along the Gulf Coast is creating long-term demand that few investors would have predicted five years ago. Pipeline companies, royalty owners, gas processors, and infrastructure providers are all benefiting from that shift.

The result is a market where capital remains available, but only for projects and assets that can clearly demonstrate value.

Perhaps the most overlooked story is what is happening to the inventory of available opportunities.

Reuters recently reported that the U.S. shale industry's inventory of drilled-but-uncompleted wells has fallen to record lows.

*Figure 4: A drilling rig operating during sunset. Source: Wildcatters.*

That matters because future production growth will increasingly require new drilling activity rather than simply bringing existing wells online.

For operators, investors, and mineral owners, that creates a different environment than the one the industry has operated in for much of the past decade.

* Asset quality matters more.

* Operational efficiency matters more.

* Infrastructure matters more.

* And perhaps most importantly, local knowledge matters more.

The oil and gas business has always been built by people willing to look where others are not.

The headlines may focus on billion-dollar mergers, major LNG terminals, and public company earnings calls.

But across the country, thousands of smaller operators are still evaluating deals, raising capital, buying assets, and building businesses one well at a time.

That part of the industry remains alive and well.

### Why It Matters

Capital is returning to energy, but it is not being distributed evenly.

Large operators continue attracting institutional investment, while independent buyers are finding opportunities in producing assets, minerals, royalties, infrastructure, and niche operating strategies.

For many in the industry, the next decade may not be about drilling the most wells.

It may be about owning the right assets, in the right basin, with the right operational strategy.

### What We're Watching

* Additional upstream M&A activity

* Private equity exits and recapitalizations

* LNG infrastructure financing

* Royalty and mineral transactions

* Independent operator acquisitions

* Capital raises targeting PDP-focused strategies

* Family office participation in upstream deals

---

### Sources & References

* **Reuters**: [reuters.com/business/energy/natural-gas-spending-hit-10-year-high-2026-oil-investment-falls-iea-says-2026-05-28](https://www.reuters.com/business/energy/natural-gas-spending-hit-10-year-high-2026-oil-investment-falls-iea-says-2026-05-28/)

* **Reuters Legal**: [reuters.com/legal/transactional/us-upstream-oil-gas-dealmaking-hit-two-year-high-q1-2026-2026-05-13](https://www.reuters.com/legal/transactional/us-upstream-oil-gas-dealmaking-hit-two-year-high-q1-2026-2026-05-13/)

* **Reuters Shale Well Backlog**: [reuters.com/business/energy/record-low-us-shale-well-backlog-curbs-fast-output-gains-amid-export-surge-2026-05-29](https://www.reuters.com/business/energy/record-low-us-shale-well-backlog-curbs-fast-output-gains-amid-export-surge-2026-05-29/)

* **Enverus**: [enverus.com](https://www.enverus.com/)

* **Kroll M&A**: [kroll.com](https://www.kroll.com/)

* **Deloitte**: [deloitte.com](https://www.deloitte.com/)

* **EIA**: [eia.gov](https://www.eia.gov/)