Oil Above $80 Is Good. Oil Above $100 Changes Everything.

While crude prices remain elevated, energy forecasts vary widely from $60 to $100 per barrel. We analyze how capital returns selectively, the growing margins of independent operators, and what happens when U.S. shale faces record-low backlogs.

For much of the past decade, the oil industry has operated under a simple assumption: capital would remain scarce, investors would demand discipline, and operators would be forced to do more with less.

Today, that assumption is being tested.

Crude prices remain elevated as global energy markets continue working through disruptions tied to the Middle East and ongoing uncertainty surrounding energy flows. While daily headlines focus on geopolitical events, the more important question for operators, investors, and mineral owners is what comes next.

Because oil prices alone do not determine the future of the industry.

Capital does.

According to a Reuters survey released May 29, analysts have increased their 2026 oil price forecasts for the third consecutive month. The consensus forecast now calls for Brent crude to average approximately $90.44 per barrel in 2026, while WTI is expected to average $84.63 per barrel. Just one month ago, expectations were closer to $86 Brent and $80 WTI.

Source:

https://www.reuters.com/business/energy/analysts-hike-oil-forecasts-again-energy-flows-face-slow-recovery-2026-05-29/

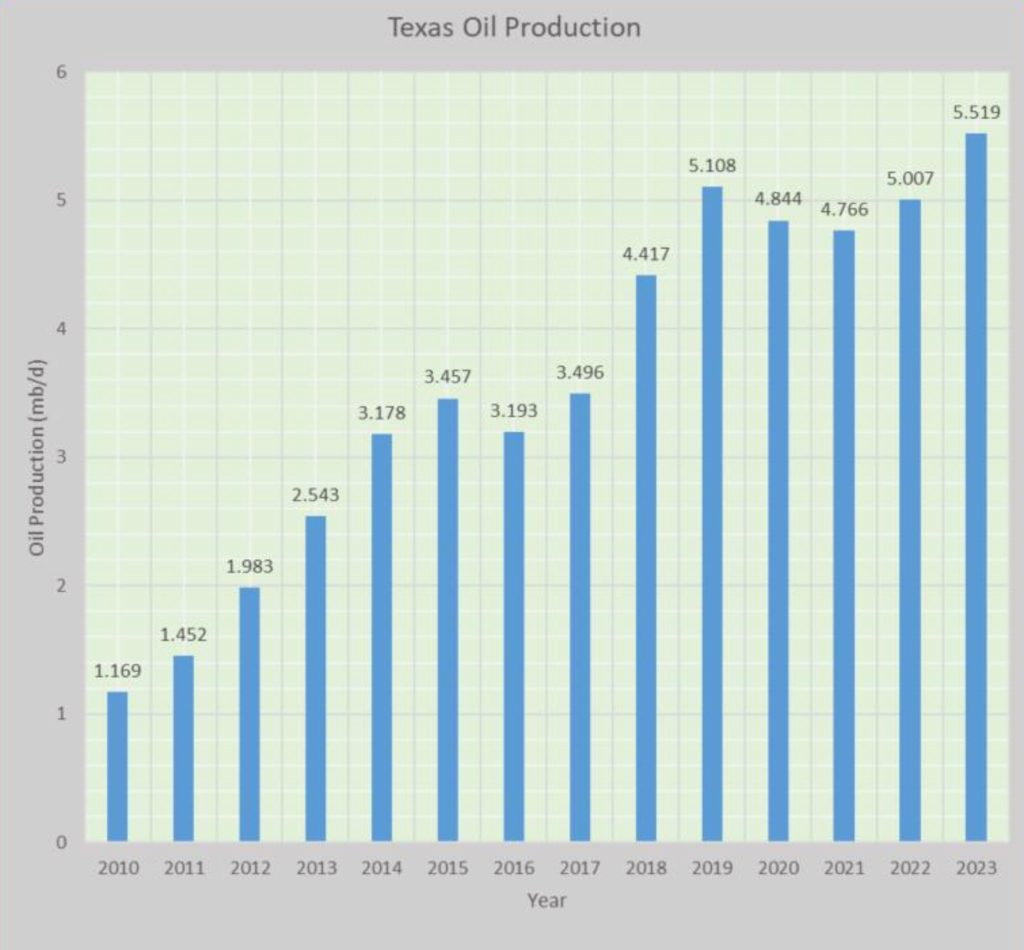

*Figure 1: U.S. and Texas crude oil production levels, showing the Permian Basin as the primary growth engine under a model of strict capital discipline. Source: Energy Data.*

Not everyone agrees.

Barclays continues to maintain one of the more bullish forecasts on Wall Street, holding a 2026 Brent forecast of $100 per barrel while warning risks remain skewed to the upside.

Source:

https://www.reuters.com/business/energy/barclays-keeps-100-brent-oil-forecast-2026-risks-skew-higher-2026-05-22/

Meanwhile, JPMorgan remains considerably more cautious, arguing that growing global supply and slowing demand could ultimately push Brent crude closer to $60 per barrel over the next several years.

Source:

https://www.jpmorgan.com/insights/global-research/commodities/oil-prices

The wide gap between those forecasts highlights the uncertainty facing the industry today.

On one side sits a world dealing with geopolitical instability, constrained inventories, and growing energy security concerns.

On the other sits a market facing slower economic growth, persistent inflation pressures, elevated interest rates, and growing questions about long-term demand.

For independent operators across Texas, Oklahoma, Louisiana, New Mexico, and Appalachia, those macroeconomic pressures matter.

Interest rates remain well above levels seen during the shale boom years. Borrowing costs have increased. Equipment costs remain elevated. Steel, labor, fuel, and service costs continue pressuring margins.

Yet something interesting is happening.

Capital is coming back.

U.S. upstream oil and gas M&A reached approximately $38 billion during the first quarter of 2026, the strongest quarter in two years according to Enverus.

Source:

https://www.reuters.com/legal/transactional/us-upstream-oil-gas-dealmaking-hit-two-year-high-q1-2026-2026-05-13/

*Figure 2: The Houston skyline at sunset, representing the central hub of energy M&A dealmaking and institutional capital deployment. Source: Energy Finance.*

The return of capital is not being driven by speculative drilling programs.

Investors are pursuing cash flow.

PDP packages.

Minerals.

Royalties.

Infrastructure.

Water assets.

Gas gathering systems.

Non-operated interests.

In other words, investors appear more interested in durable margins than production growth.

And that raises an uncomfortable question.

Are oil prices really driving profits?

Or is the industry simply becoming better at extracting larger margins from every barrel produced?

Over the past several years, major operators have dramatically improved operational efficiency. Longer laterals, better completion designs, improved drilling technology, and stricter capital discipline have lowered breakeven costs across much of the shale patch.

Many Permian operators can now generate attractive returns at oil prices that would have been considered challenging a decade ago.

The result is a business model where profitability increasingly depends on operational execution rather than simply hoping for higher commodity prices.

That trend may explain why large operators continue generating record cash flows even during periods when oil prices are not setting records.

Meanwhile, overseas discoveries continue reshaping the global competitive landscape.

Guyana remains one of the most important oil discoveries in modern history, with ExxonMobil continuing to expand development activity across the Stabroek Block. Additional offshore discoveries in Guyana, Brazil, Namibia, and Trinidad continue attracting billions of dollars in long-term investment.

Those projects matter because they represent future supply growth that will eventually compete with U.S. shale production.

For now, however, U.S. producers retain one critical advantage.

Speed.

An offshore project may take seven to ten years to develop.

A shale well can often move from permitting to production in a fraction of that time.

That flexibility continues making U.S. operators one of the world's most important swing producers.

### What About the Mom-and-Pop Operators?

The future of American oil and gas will not be decided exclusively in Houston boardrooms.

Thousands of independent operators continue producing meaningful volumes across mature fields throughout the country.

Many of these businesses are family-owned.

Some operate fewer than 100 wells.

Others manage mineral portfolios, royalty interests, or non-operated working interests accumulated over decades.

These operators face challenges that large public companies often do not.

Higher financing costs.

Smaller technical teams.

More limited access to capital.

Greater exposure to commodity volatility.

Yet they also possess advantages.

Local knowledge.

Operational flexibility.

Lower overhead.

Direct relationships with landowners and communities.

*Figure 3: Silhouette of land-drilling pumpjacks operating in mature U.S. oil fields, the operational domain of independent operators. Source: Field Operations.*

As capital returns to energy, many investors are beginning to recognize that smaller operators often generate attractive risk-adjusted returns through disciplined acquisitions rather than large-scale drilling programs.

That trend could become one of the more overlooked stories in the industry over the next several years.

### Why It Matters

The biggest story in energy right now is not oil prices.

It is the battle between price, profitability, and capital.

If oil remains above $80, most of the industry can survive.

If oil remains near $90 to $100, acquisition activity, capital raises, and infrastructure investment are likely to accelerate.

But the winners may not simply be the companies producing the most barrels.

The winners may be the companies generating the highest margins on every barrel they produce.

### What We're Watching

• WTI holding above $80 per barrel

• Additional upstream capital raises

• Private equity re-entering oil and gas

• Permian Basin acquisition activity

• LNG infrastructure investment

• Guyana and offshore development growth

• Independent operator acquisition opportunities

• Interest rate policy and its impact on energy financing