Oil Is Rising. Capital Is Returning. But the Biggest Opportunity May Not Belong to Big Oil.

WTI prices climb and capital returns selectively to energy, but major public consolidation leaves valuable non-core opportunities. We analyze record-low DUC backlogs and the natural gas investment boom.

For most of the past decade, it has been difficult to bet against scale in the oil business.

The largest operators controlled the best acreage. They had the lowest cost of capital. They owned the infrastructure. They had access to public markets, private equity, and investment banks. When commodity prices weakened, they could survive longer than everyone else.

The shale era rewarded size.

But something interesting has happened over the past several months.

The advantages that helped build the largest companies in the industry are no longer expanding at the same pace.

Meanwhile, a different set of advantages is beginning to matter again.

Relationships.

Local knowledge.

Asset selection.

Cash flow.

Patience.

In other words, many of the characteristics that have historically defined independent operators.

This week's headlines tell that story surprisingly well.

The most visible headline came from global oil markets.

Crude prices pushed higher after renewed concerns about Middle East supply disruptions and the potential impact of shipping constraints through the Strait of Hormuz. Reuters reported that traders continued pricing in supply risk even as broader economic concerns lingered.

Source:

https://www.reuters.com/business/energy/oil-rises-2-iran-announces-closure-strait-hormuz-following-us-strikes-2026-06-11/

Normally, higher oil prices would be enough to trigger another drilling boom.

That has not happened.

Instead, operators have remained remarkably disciplined.

Part of the reason is economic.

The cost of capital today is dramatically different than it was during the last major shale expansion. Interest rates remain elevated. Lenders are more selective. Investors are demanding returns rather than production growth.

Higher oil prices help, but they do not erase financing costs.

At the same time, operators are facing a reality that few people outside the industry appreciate.

The easiest barrels have already been drilled.

Reuters reported this month that drilled-but-uncompleted well inventories across U.S. shale basins have fallen to record lows.

Source:

https://www.reuters.com/business/energy/record-low-us-shale-well-backlog-curbs-fast-output-gains-amid-export-surge-2026-05-29/

For years, these DUC inventories acted as a hidden reserve of future production. When prices improved, operators could quickly complete existing wells and bring production online.

Today, much of that inventory is gone.

Future growth requires fresh capital.

Fresh drilling.

Fresh risk.

That changes the economics of the business.

It also changes the opportunities.

While public investors focus on Exxon, Chevron, and the largest public operators, another market has quietly become more active.

The private market.

According to Enverus data reported by Reuters, U.S. upstream dealmaking reached $38 billion during the first quarter, the strongest quarter in two years.

Source:

https://www.reuters.com/legal/transactional/us-upstream-oil-gas-dealmaking-hit-two-year-high-q1-2026-2026-05-13/

The headline transactions involved billion-dollar mergers.

The more interesting activity is occurring beneath those headlines.

As operators grow larger, they create more non-core assets.

A package producing a few hundred barrels a day may not matter to a billion-dollar public company. It may matter tremendously to a private operator.

A scattered mineral package may be too small for an institutional buyer.

It may be ideal for a family office.

A mature field with stable production may not fit a growth-focused public company.

It may generate attractive returns for a local operator who understands every well on the lease.

That is where many of today's opportunities are emerging.

Not because the assets are new.

Because the buyers are different.

This shift is particularly important for brokers and landmen.

The public market likes efficiency.

The private market still runs on information.

The broker who knows an owner is considering a sale.

The landman who identifies fragmented mineral ownership.

The operator who understands a mature field better than anyone else.

Those advantages are difficult to model in a spreadsheet, but they remain valuable.

Perhaps increasingly valuable.

Meanwhile, another trend is reshaping the capital landscape.

Natural gas.

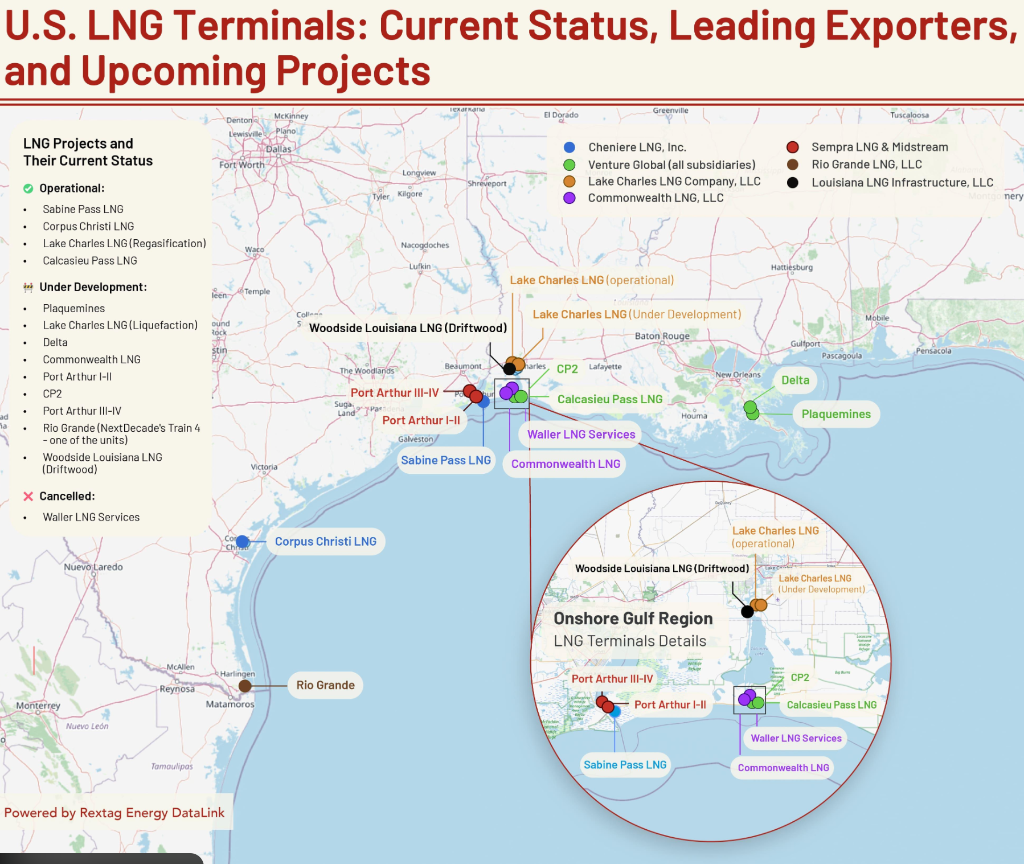

One of the biggest energy stories this year has not been oil. It has been LNG.

The International Energy Agency expects global natural gas investment to reach its highest level in more than a decade as countries continue investing in energy security and supply diversification.

Source:

https://www.reuters.com/business/energy/natural-gas-spending-hit-10-year-high-2026-oil-investment-falls-iea-says-2026-05-28/

*Figure 1: Current status of operational and upcoming U.S. LNG terminal projects. Global natural gas and LNG investment is reaching a 10-year high, driven by countries prioritizing long-term energy security. Source: Rextag Energy DataLink.*

That investment is creating opportunities across the Gulf Coast, the Haynesville, Appalachia, and other gas-focused regions.

This week Reuters reported commodities trader Gunvor is backing a private company to acquire U.S. natural gas assets, another signal that sophisticated investors continue positioning around long-term gas demand.

Source:

https://www.reuters.com/legal/litigation/commodities-trader-gunvor-funds-venture-buy-us-natural-gas-production-2026-06-10/

The takeaway is not that another shale boom is coming.

It is that capital is returning selectively.

Investors want assets.

They want cash flow.

They want infrastructure.

They want exposure to long-term energy demand.

What they do not want is reckless growth.

That distinction may define the next phase of the U.S. oil and gas industry.

The last cycle rewarded companies that could drill the fastest.

The next cycle may reward those who know how to buy the right assets, structure the right deals, and operate efficiently in a more disciplined market.

For independent operators, brokers, landmen, and investors, that may be the most important headline of all.