Texas Pipeline Expansion Gains Urgency as LNG Demand Surges

New pipeline construction across Texas is becoming increasingly important as global LNG markets remain under pressure following continued disruptions tied to the Middle East conflict.

New pipeline construction across Texas is becoming increasingly important as global LNG markets remain under pressure following continued disruptions tied to the Middle East conflict.

According to the EIA, developers plan to bring approximately **44.9 Bcf/d of new natural gas pipeline capacity online** across the United States in 2026 and 2027. More than **66% of that expansion originates in Texas**, largely tied to Permian takeaway capacity and LNG export demand.

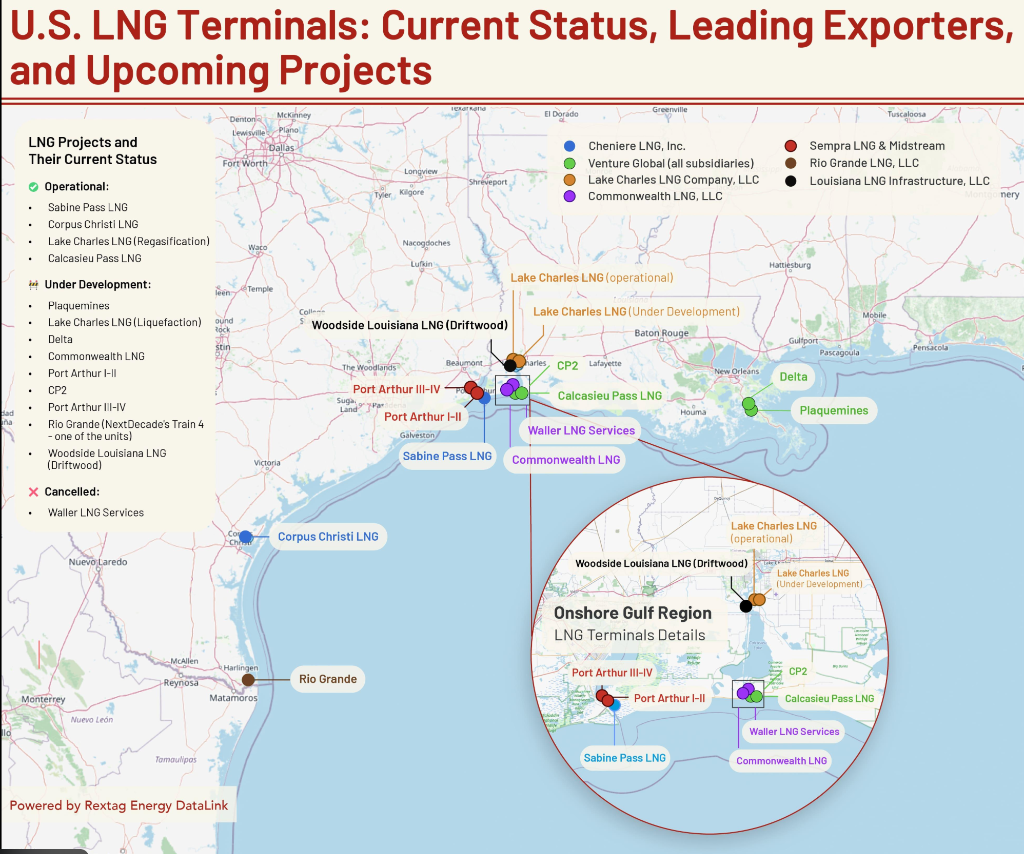

*Figure 1: Current and planned U.S. LNG terminals, the ultimate destinations for Texas natural gas pipeline expansions. Source: EIA Today in Energy.*

## The Timing Matters

Reuters reported this week that LNG buyers across Asia are accelerating long-term supply discussions with U.S. exporters after damage to Qatar’s Ras Laffan LNG infrastructure disrupted roughly **17% of global LNG export capacity**.

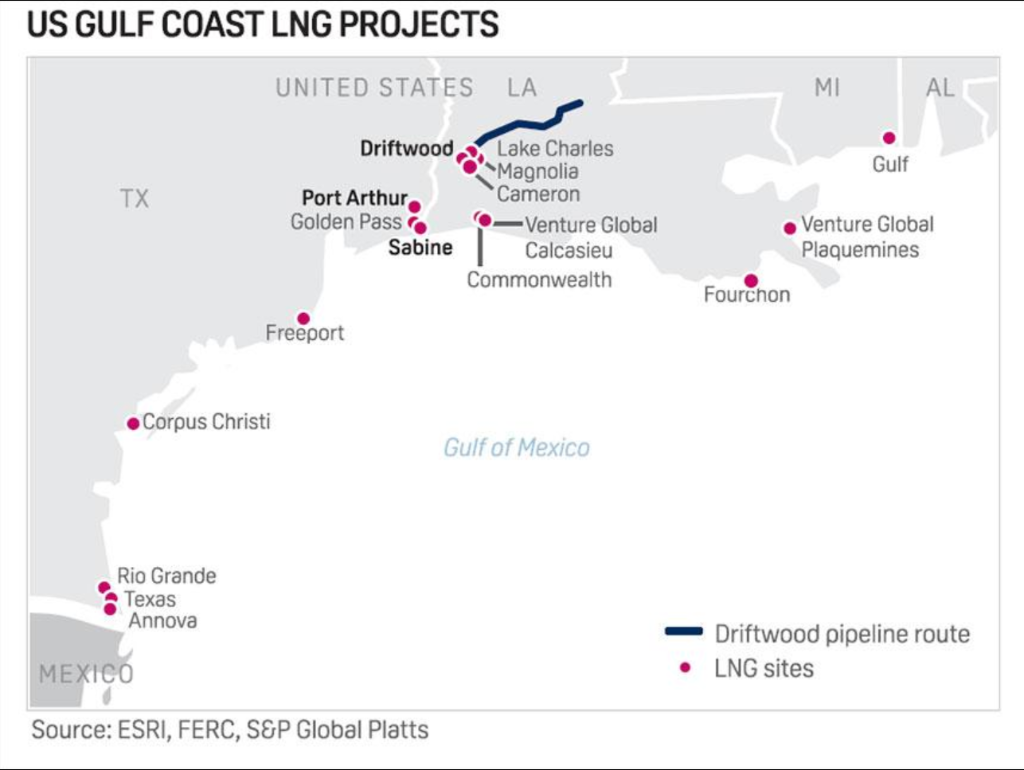

*Figure 2: Major LNG export terminals along the U.S. Gulf Coast driving long-term demand and midstream commitment. Source: Market Intelligence.*

At the same time, Permian operators continue dealing with regional gas takeaway constraints, leading to high price volatility at the Waha hub. For midstream developers, these overlapping drivers—rapid international demand growth and Permian production pressures—have turned Texas midstream additions into a critical infrastructure bottleneck.

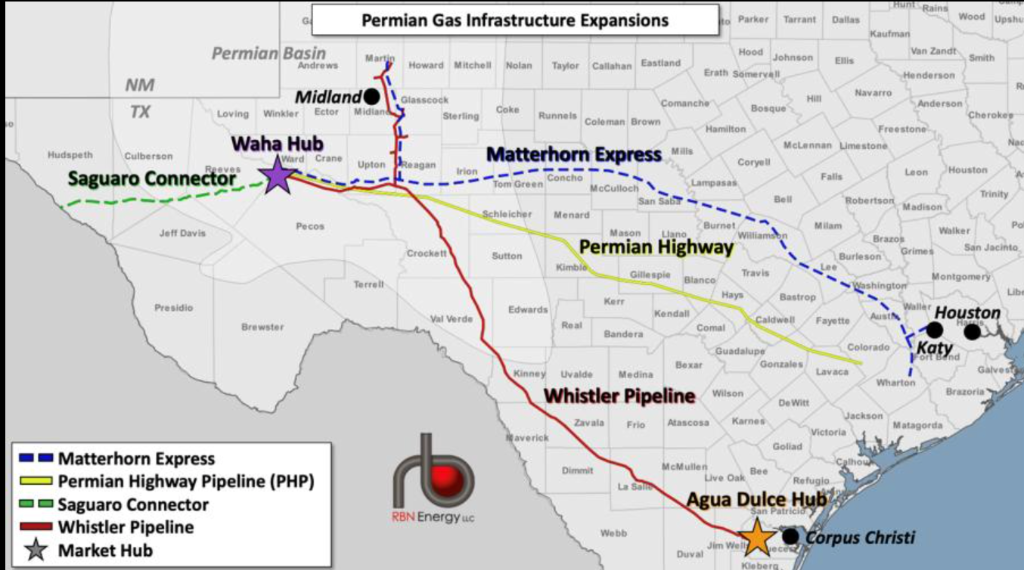

*Figure 3: Current Permian Basin natural gas takeaway infrastructure and planned links to Gulf Coast demand centers. Source: EIA.*

## Key Projects Driving Near-Term Relief

Three projects are set to provide critical near-term relief to West Texas operators and Gulf Coast exporters alike:

1. **Gulf Coast Express (GCX) Expansion**: Adding **0.57 Bcf/d** of capacity, expected online in mid-2026.

2. **Blackcomb Pipeline**: A major greenfield line adding **2.5 Bcf/d**, expected online in late 2026.

3. **Matterhorn Express Pipeline**: Another massive addition of **2.5 Bcf/d**, expected online by late 2026.

Together with planned expansions at existing Texas LNG terminals like Freeport LNG and Port Arthur LNG, these lines represent the backbone of the next phase of Gulf Coast energy exports.

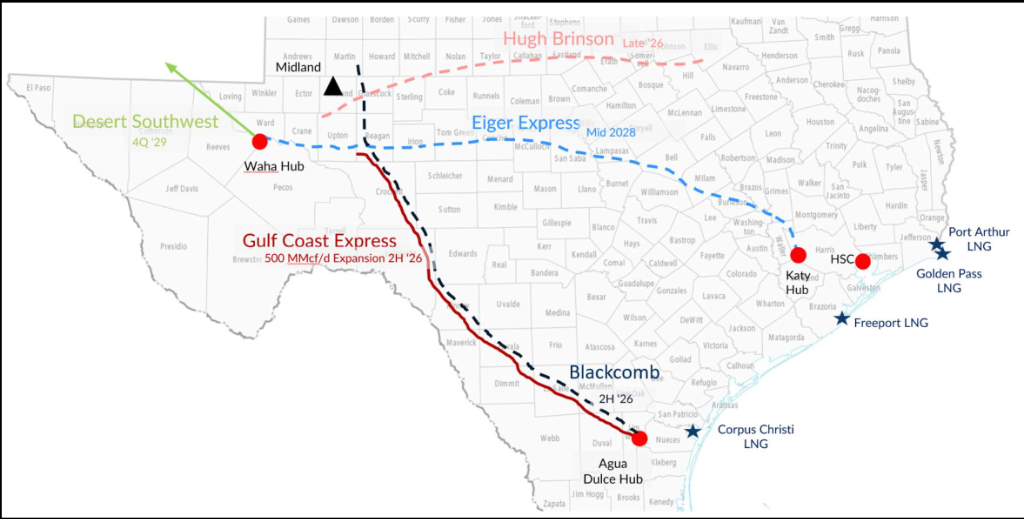

*Figure 4: Detailed routing of pipeline expansions linking Waha pricing hubs directly to Gulf Coast liquification plants. Source: Industry Map.*

For operators and investors, securing capacity along these key corridors has become the primary focus of the 2026 midstream cycle. As physical takeaway constraints are eased, West Texas operators will be positioned to increase production without fear of negative Waha pricing, while global buyers secure reliable, long-term U.S. shale-sourced molecules.

---

### Sources & References

- **U.S. Energy Information Administration (EIA)**: [eia.gov/todayinenergy](https://www.eia.gov/todayinenergy/detail.php?id=67624)

- **Reuters Energy**: [reuters.com/business/energy](https://www.reuters.com/business/energy/us-thailand-speed-lng-talks-war-hits-qatar-exports-sources-say-2026-05-26/)

- **Midland Reporter-Telegram Energy**: [mrt.com/business/oil](https://www.mrt.com/business/oil/article/texas-oil-gas-production-report-22277351.php)