Why Independent Operators May Be Better Positioned Than They Think and Why is Oil going to stay near $100 vs $70?

As the energy market shifts from oversupply concerns to energy security, independent operators find themselves uniquely positioned. We analyze why oil is poised to stay near $100, the collapse of DUC backlogs, and record natural gas investments.

The biggest story in energy right now is not simply that oil prices are high.

It's that the world is increasingly willing to pay a premium for energy security.

For the better part of the last decade, oil and gas companies operated in a market dominated by oversupply concerns, investor skepticism, and growing pressure to reduce spending. Today, that environment is changing. Geopolitical instability, tighter inventories, growing LNG demand, and a renewed focus on domestic energy production have reshaped how investors view the sector.

The result is a market where capital is beginning to return, but not evenly.

According to the U.S. Energy Information Administration, global oil inventories are expected to continue falling throughout 2026 following significant disruptions to Middle East production and shipping routes. The EIA estimates global inventories could decline by 2.6 million barrels per day this year, helping keep Brent crude prices elevated despite recent volatility.

Source:

https://www.eia.gov/outlooks/steo/

The agency expects Brent crude to average roughly $106 per barrel during the current period before moderating later in the year as supply gradually recovers.

That outlook stands in contrast to only a year ago, when many analysts were forecasting a prolonged period of lower prices.

Yet despite stronger commodity prices, the industry has not returned to the "drill at all costs" mentality that defined previous booms.

Instead, operators are pursuing a different strategy.

Generate cash flow.

Protect margins.

Acquire quality assets.

Avoid overextending balance sheets.

That discipline is one reason U.S. upstream M&A activity reached a two-year high earlier this year as buyers targeted producing assets rather than speculative growth opportunities.

Source:

https://www.reuters.com/legal/transactional/us-upstream-oil-gas-dealmaking-hit-two-year-high-q1-2026-2026-05-13/

## The Global Story: Energy Security Is Driving Investment

The global energy landscape has shifted dramatically over the past several years.

Europe continues searching for alternatives to Russian energy supplies.

Asian importers are competing aggressively for LNG cargoes.

Middle East disruptions have reminded governments that supply security still matters.

As a result, energy investment is increasingly flowing toward projects that provide reliability.

The International Energy Agency recently reported that global investment in natural gas projects is expected to exceed $330 billion in 2026, the highest level in more than a decade.

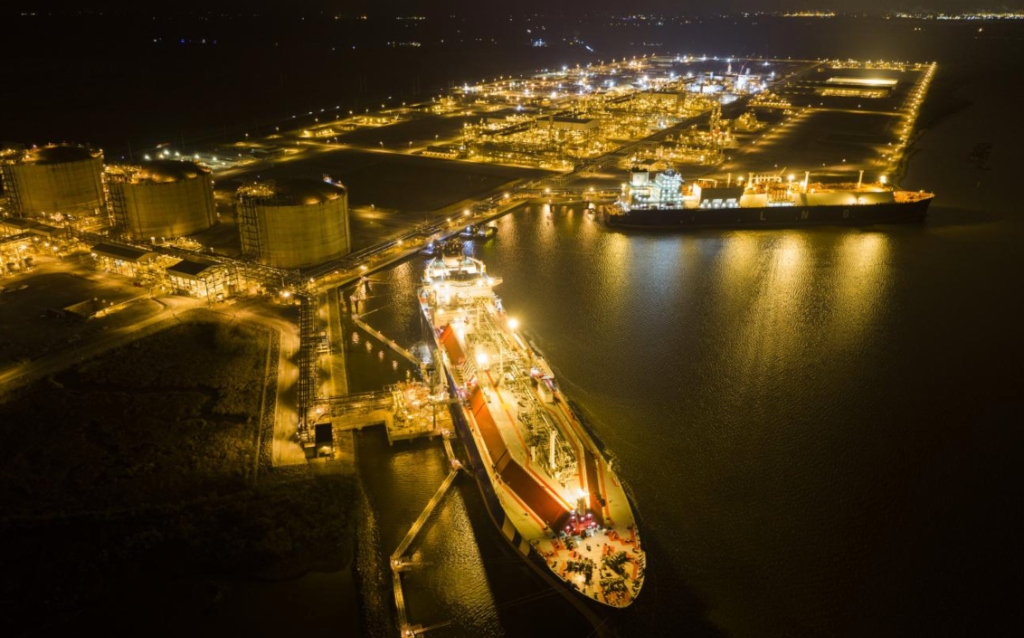

Source:

https://www.reuters.com/business/energy/natural-gas-spending-hit-10-year-high-2026-oil-investment-falls-iea-says-2026-05-28/

Much of that spending is tied directly to LNG.

The United States continues expanding export capacity along the Gulf Coast, positioning itself as one of the world's most important suppliers of natural gas. Industry forecasts discussed at Reuters' Global Energy Forum suggest global LNG demand could increase by as much as 60% by 2040.

Source:

https://events.reutersevents.com/energy-transition/global-energy-transition-new-york/agenda

*Figure 2: A major Gulf Coast liquefaction facility loading LNG tankers at night. Global natural gas investment is hitting a 10-year high, driven by long-term security of supply. Source: Infrastructure Intelligence.*

This matters because LNG has become more than a commodity.

It has become a geopolitical tool.

Countries increasingly view access to reliable LNG supplies as a national security issue, creating long-term opportunities for producers, infrastructure companies, and investors.

## The National Story: Higher Prices, But a More Disciplined Industry

The U.S. energy sector is benefiting from higher prices, but operators face a different set of challenges than they did during previous cycles.

Labor remains expensive.

Service costs remain elevated.

Interest rates remain significantly higher than the near-zero environment that fueled much of the shale boom.

At the same time, shale producers have quietly exhausted one of their most important buffers.

Reuters recently reported that drilled-but-uncompleted wells, commonly known as DUCs, have fallen to record lows across the industry.

Source:

https://www.reuters.com/business/energy/record-low-us-shale-well-backlog-curbs-fast-output-gains-amid-export-surge-2026-05-29/

*Figure 1: A U.S. land drilling rig operating at sunset. With drilled-but-uncompleted (DUC) well inventories at record lows, future production growth will require sustained new drilling activity and capital. Source: Field Operations.*

For years, these wells provided operators with a relatively low-cost way to increase production when prices improved.

Today, that inventory has largely disappeared.

Future growth will require fresh drilling capital.

That reality is becoming increasingly important as global inventories tighten and demand remains resilient.

In other words, the next barrel may cost more to produce than the last.

## Why This Matters for Independent Operators

This is where the story becomes particularly interesting.

Public markets continue focusing on mega-mergers, LNG terminals, and billion-dollar projects.

But much of the activity occurring across the oil patch is happening far below that level.

Family offices are buying producing assets.

Private investors are acquiring minerals.

Small operators are pursuing PDP packages.

Regional groups are assembling acreage positions.

Brokers are sourcing off-market opportunities.

Landmen are identifying fragmented ownership positions that larger companies often overlook.

The economics make sense.

Large operators need transactions measured in hundreds of millions of dollars to move the needle.

Independent operators can create significant value from much smaller opportunities.

A producing asset generating stable cash flow.

A mineral package in a proven basin.

A water disposal business serving existing production.

These opportunities may never appear in a Wall Street research report, but they remain the backbone of much of the domestic energy industry.

As consolidation continues among public companies, more assets become non-core.

And every non-core asset eventually becomes someone else's opportunity.

## Raising Capital in Today's Market

The biggest mistake many operators make is assuming investors are looking for production growth.

Most are not.

Investors today are looking for predictability.

The capital raising environment has fundamentally changed.

Five years ago, a growth story could attract funding.

Today, investors want to see:

• Existing cash flow

• Low decline rates

• Conservative leverage

• Operational discipline

• Clear exit opportunities

• Infrastructure access

• Strong management teams

For independent operators, this creates both challenges and opportunities.

Debt is more expensive than it was during the shale boom.

Equity investors are more selective.

However, quality assets continue attracting capital.

In many cases, operators are finding success by emphasizing cash-on-cash returns rather than production growth projections.

Investors have become much more interested in free cash flow than forecasts.

That trend favors operators who understand their assets deeply and can articulate a clear path to returns.

## The Bottom Line

The energy market is entering a new phase.

Oil prices remain elevated.

Global inventories are tight.

Natural gas investment is accelerating.

Capital is returning to the sector.

But the winners may not be the companies producing the most barrels.

The winners may be the operators, investors, brokers, and land professionals who understand how to create value in a market increasingly focused on cash flow, energy security, and disciplined growth.

The next energy cycle is unlikely to look like the last one.

And for many independent operators, that may be a good thing.

### Key Reads

EIA Short-Term Energy Outlook

https://www.eia.gov/outlooks/steo/

Reuters: Global Oil Inventories Running Dangerously Low

https://www.reuters.com/business/energy/global-markets-oil-analysis-pix-2026-06-05/

Reuters: Natural Gas Investment Hits 10-Year High

https://www.reuters.com/business/energy/natural-gas-spending-hit-10-year-high-2026-oil-investment-falls-iea-says-2026-05-28/

Reuters: U.S. Upstream M&A Hits Two-Year High

https://www.reuters.com/legal/transactional/us-upstream-oil-gas-dealmaking-hit-two-year-high-q1-2026-2026-05-13/

Reuters: Record Low DUC Inventory

https://www.reuters.com/business/energy/record-low-us-shale-well-backlog-curbs-fast-output-gains-amid-export-surge-2026-05-29/